As we enter the new millennium, economic growth and technological progress seem to be promising in most developing countries. However, whether their existing energy systems will support a fast-growing economy remains a crucial question for policy makers.

Enviromnental damage ramains a growing concern. Despite rigorous energy efficiency programs and research and development (R&D) efforts on cleaner energy technologies in most developed countries, no developing country views these as priorities. And they have a case: Developed countries, which enjoyed high economic growth for decades by ignoring the environmental consequences, are hindering developing countries’ economic growth. On the other hand, representatives from developed countries say that we are all in the same boat and will sink together if developing countries do not pay attention to environmental consequences.

In December 1997, world leaders gathered in Kyoto to address the problem of global warming and to decide which countries should cut emissions and to what extent. Not surprisingly, developing countries objected to any restriction that might limit their economic growth. Such discussions will become more intense in the aftermath of the Kyoto Protocol.

This article will not address the issue of environmental reparations. Rather, it will discuss the energy markets’ current situation and short-term future trends.

Basic Properties of the Energy Systems

Present-day energy systems have several basic characteristics. All policy makers dealing with energy systems should know these basics by heart.

First, energy systems develop slowly because they require significant capital and infrastructure that can be replaced only gradually. There are two important consequences resulting from this fact:

•Intense capital requirements are a strong barrier to average-sized firms. Thus, energy systems are seldom run by private enterprises. In most countries they are constructed and run by the state, and a separate government body deals with energy issues. Energy systems have been dominated by heavy regulations even in most market-oriented economies. The recent trend of deregulation is an exception rather than the norm.

•Even if a state realizes that current energy systems can be improved significantly (e.g., switching to other fuel types or deregulating the market), making changes to a huge, functioning infrastructure is a slow and painful process. It is relatively easy to make changes during the initial stages of an energy system. But as time passes, this becomes more difficult.

As in most cases, good planning is essential. A state must be very careful when building its energy systems, and should pay attention to underlying energy market trends. Important lessons can be learned from the long history of mistakes committed by developing countries. And if a developing country fails to keep up with recent trends, it may find itself trapped by its own hands in an inherently inefficient system for decades.

Second, energy systems are heavily reliant on fossil fuels. Historically, coal has been a prominent energy resource in most countries. Despite its widely acknowledged negative impact on human health and the environment, it still dominates energy systems in such developing countries as India and China. In most countries, oil is the primary energy source.

Oil was one of the most influential key factors of the twentieth century. Just by looking at the traffic on our teeming highways or the modern political landscape, we can understand how profoundly oil has changed the way we live and handle international politics. In the light of the oil crises of 1973 and 1980, the reverse-shock of 1986, and another crisis during the Gulf War of 1990, the need to diversify away from oil becomes abundantly clear.

Environmental concerns also support the case against oil. This is how natural gas, a slightly cleaner fossil fuel, gradually entered the picture. Given the current energy systems’ dependence on these fossil fuels and the fact that energy systems change slowly, oil, coal and natural gas will continue to be dominant for years.

Third, the driving force behind the dynamic of switching from one fuel type to another is economics. Fuel types with smaller unit costs survive in the long run. Oil, for example, now has the lowest unit cost (cost per unit of energy) in most regions of the world.1

Given this, cleaner fuel (e.g., solar energy) still have a long way to go before becoming economically viable. Why would you pay $5 for what you can get for $3? Countries that use non-oil energy resources do this for a number of reasons, such as they do not have natural resources and so transporting oil ends up costing more, or they have abundant natural energy resources of other types. But, in general, economics is the most important issue here.

Introducing New Fuels

What trajectory does the unit cost follow when a new fuel is introduced? Consider photovoltaic (PV) cells. The term photovoltaic refers to a family of technologies that convert light directly into electricity. PV technology is an appealing alternative-it is a renewable, environmentally benign, and domestically secure energy source. It is modular and can be scaled up to meet demand.2 However, unit cost is currently high compared to fossil fuels.

A new technology’s unit cost is believed to follow a learning (or experience) curve as a function of installed capacity. As shown in Figure 1, technologies may experience declining costs due to their increasing adoption by society. This decline may be attributed to several factors:

• Technology innovation and manufacturing improvements: Costs may decline due to a better understanding of the underlying science, progress in related fields, or via learning by doing as well as learning by using.

• Economies of scale: Unit cost is a function of total production. Products produced in large quantities have lower unit costs. Most new fuel types have high unit costs, and demand is too low to encourage large-scale production. It almost seems paradoxical. But there are ways to break this cycle. Regulations encouraging usage of new fuel types may be enforced, consumers who have priorities other than cost may be targeted to expand the current market, or the cost may drop low enough for the technology to become attractive even for low production levels.

In achieving economies of scale, consumer demand should he considered. A major concern for the end-use consumer is convenience. The value of oil would be much lower if gas stations were not located all over the country. The same issue applies to fuel cells and electric cars. They will not be as convenient as conventional cars until the proper infrastructure exists.

Since 1960s, cooperative investments by manufacturers and governments have resulted in the accumulation of experience within the solar industry and the subsequent cost reduction of PV systems. Significant cost reductions have occurred in both the PV modules that house the solar cells, and the ancillary components (known as balance-of-system). Between 1968 and 1998, the global cumulative installed capacity of PV modules doubled more than thirteen times, from 95 kW to 950 MW, while costs ($/Wp) were reduced by an average of 20.2% for each doubling.4

Trends for Different Fuel Types

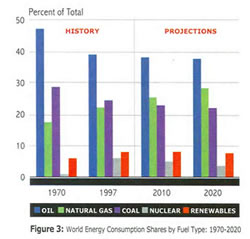

After this overview of energy systems, lets look at the trends for specific fuel types. Figure 2 is taken from International Energy Outlook 2000 (IEO2000), an annual report published by the U.S. Energy Information Administration (EIA).5 It displays projections of energy usage by fuel type up to 2020. The highlights following the figure are summarized from the reports contents.

Coal: Carbon dioxide is a very effective greenhouse gas and contributes significantly to global warming. Since coal is the most carbon-intensive fuel, global climate change debates focus on reducing its use. Coal use also has significant public health consequences, due to particulate matter emissions. Historically, coal has been a major source of energy. Although it has lost market share to petroleum products, natural gas, and nuclear power in the last decades, it remains a key source of energy, especially for generating electricity. In the IEO2000 reference case, coals share of total energy consumption falls only slightly, from 24 percent in 1997 to 22 percent in 2020 (Figure 3). Its historical share is nearly maintained, because large increases in energy use are projected for developing Asian countries, where coal continues to dominate many national fuel markets. China and India are projected to account for 97 percent of the worlds total increase in coal use.

Oil: Oil use will grow in absolute terms, but even optimistic oil supply scenarios predict that its share in the fuel mix will decline gradually. Despite efforts to reduce reliance on Middle Eastern oil, as well as advances in technical capability, new oil reserves are not compensating for depleted ones. The experts estimates of vast oil reserves in the Caspian and Tarim basins proved to be somewhat high, and the latest probes have been partially disappointing. According to EIA estimates, the share of the Persian Culf supplies is likely to increase in the coming years. Economic theory says that prices rise as supply declines. Oil prices have been quite volatile and can be expected to remain so in the future, principally as the result of unforeseen political and social circumstances. Without attempting to predict any crisis, the IEO2000 forecast shows a gradual rise in world oil prices. Oil currently provides a larger share of world energy consumption than any other energy source and is expected to remain in that position throughout the forecast period. Its share of total energy consumption declines slightly, however, from 39 percent in 1997 to 38 percent in 2020, as countries in many parts of the world switch to natural gas and other fuels, particularly for electricity generation. World oil consumption is projected to increase by 1.9 percent annually over projection period. Most of the growth in oil use is projected for the transportation sector, where few alternatives are currently economical.

Natural Gas: Natural gas remains the fastest growing component of global energy consumption. Over the IEO2000 forecast period, its use is projected to more than double in the reference case, reaching 167 trillion cubic feet. The natural gas share of total energy consumption increases from 22 percent in 1997 to 29 percent in 2020. It also accounts for the largest increment in electricity generation. Combined-cycle gas turbine power plants offer some of the highest commercially available plant efficiencies, and natural gas is environmentally attractive because it emits less sulfur dioxide, carbon dioxide, and particulate matter than either oil or coal.

|

| World Energy Consumption Shares Type: 1970-2000 |

In the industrialized world, natural gas consumption has the largest projected increase among the major fuels, increasingly becoming the choice for new power generation because of its environmental and economic advantages. Its incremental use in developing countries is expected to supply both power generation and other uses, such as town gas and fuel for industry. Despite concerns about the extent of natural gas reserves worldwide, current proven reserves suffice for this markets steady development without a substantial price increase.

Nuclear Power: The prospects for nuclear power are uncertain, despite a projected growth rate of 2.5 percent per year in total electricty demand through 2020. In the IEO2000 reference case, global nuclear capacity is projected to increase to 368 gigawatts in 2010 and then gradually fall to 303 gigawatts in 2020. Aggressive plans to expand nuclear capacity, mainly in Asia, lead to a near-term increase. However, plant retirements in America and other countries exceed total new additions worldwide, and produce a decline later in the forecast. The International Institute for Applied Systems Analysis [IIASA] is one of the authorities on energy issues.

IIASA projections [which extend until 2100] hold a slightly pessimistic view of nuclear energy. Nuclear energy production has stagnated for several decades, and IIASA suggests that this will continue. Currently, nuclear energy is prominent in only a handful of countries. Not many nuclear plants are being built, and existing ones are being dismantled. With large up-front capital costs, plant safety, and recycling nuclear material after dismantling issues, this option is becoming less and less attractive. Public opposition, already strong in the US and Europe, is growing in Asia. Nuclear safety issues moved to the forefront in Asia in 1999 after several leaks at nuclear power plants in South Korea and China, and the serious accident in a reprocessing facility in Tokaimura, Japan. Such events are likely to raise concerns about Asias aggressive plans for nuclear capacity expansion. IIASA predicts that if a safer and cheaper new generatinn of nuclear plants is introduced, nuclear powers ultimate share in fuel mix will grow. Otherwise, it eventually will come to an end.

Renewables: The development of renewable resources is constrained in the IEO2000 reference case projections by expectations that fossil fuel prices will remain relatively low, and that, as a result, renewables will have a difficult time competing. Failing a strong global commitment to environmental programs, such as the limitation and reduction of greenhouse gases outlined in the Kyotu Protocol, it is difficult to foresee significant and widespread increases in renewable energy use. Modest growth in renewabte energy is projected to continue, maintaining an 8 percent share of total energy consumption. Nevertheless, in the long run, as other fossil fuel types become more expensive due to depletion and R&D efforts push the unit cost further down, new opportunities will emerge. Even conservative estimates predict that the worlds energy will rely considerably on renewables before 2100.7

Conclusion

In this article,we highlighted several basic characteristics of energy systems, and drew attention to some underlying trends for particular fuel types. Based on this information, we can say that:Energy systems are capital-intensive and hard to change once they have been built. Therefore, developing countries should track energy system trends closely and build their energy systems according to their future needs. The most important factor influencing the decision of which energy source to use is economics. Until a resources unit cost is competitive with others, it will not enjoy widespread acceptance and usage. Fossil fuels will dominate energy markets in the short run. The shares of coal and oil in the fuel mix will remain relatively constant until 2020, while the market for natural gas will expand rapidly. Nuclear power will survive only if a new generation of safer and cheaper reactors is introduced. Renewables will be the ultimate choice of the future. Currently, however, they cannot compete successfully on cost with conventional fuels.

Footnotes

- Although the cost of extraction rises as the amount of oil remaining underground decreases, extraction technology also advances and pushes the cost down. Transporting oil from the field to the marketplace is added to the extraction (or purchasing) cost.

- Christopher Harmon, Experience Curves of Photovoltaic Technology (March 2000). The entire report is available on IIASA web site: http: www.iiasa.ac.at/Publications/Documents lR-00-014.pdf

- Netherlands Energy Research Foundation (ECN at Petten), “Endogenous Technological Change in Energy System Models.” Paper presented at the 1999 IIASA conference.

- IIASA-WEC. 1998.

- International Energy Outlook 2000 is available on the EIAs Web site: http: www.eia.doe.gov/oiaf/ieo/index.html.

- N. Nakicenovic, A. Gruebler, and A. McDonald, Global Energy Perspectives (Cambridge. UK: 1998).

- Experts differ over what exactly is included in this category. For practical purposes, renewables cover all energy sources except coal, oil, natural gas, and nuclear. Therefore this group includes, but is not limited to, hydroelectricity, wave, wind, biomass, and solar energy.